Imagine you are looking at a company's financial health like a doctor looks at a patient's chart. You don't need to be a surgeon to understand if the patient is stable or in critical condition. An audit report is an independent assessment of a company's financial statements and internal controls serves exactly that purpose. It tells you whether the numbers you see are trustworthy. Most people skip this document because it looks dense and legalistic. But hiding inside those pages are the real red flags-or green lights-that determine if your investment is safe.

In 2023, 98.7% of Fortune 500 companies required annual audits, yet many investors still struggle to decode them. The goal of this guide is simple: strip away the jargon and show you exactly where to look so you can make smarter decisions. You will learn how to spot a clean bill of health versus a warning sign, what specific phrases mean trouble, and how new regulations are changing the game.

The Anatomy of an Audit Report

To read an audit report, you first need to know its structure. These documents follow a strict format governed by standards like Generally Accepted Auditing Standards (GAAS) is a set of guidelines used by auditors when performing audits of financial statements. Whether you are looking at a U.S. public company or a global firm, the core components remain similar. The report typically starts with a title page and an executive summary, but the meat lies in four key sections mandated by bodies like the Financial Accounting Standards Board (FASB).

- The Auditor’s Report: This is the main opinion section. It states whether the financial statements are accurate.

- Management’s Responsibility: Here, the company admits they created the reports. They are responsible for the data; the auditor just checks it.

- The Auditor’s Responsibility: This explains how the audit was done. Did they check everything? No. They sampled transactions based on risk.

- The Basis for Opinion: This confirms the auditor is independent and followed the rules. If they aren't independent, the report is worthless.

As of 2026, most major firms also include Critical Audit Matters (CAMs). These are detailed explanations of the trickiest parts of the audit, such as valuing complex assets or estimating future liabilities. Pay attention here. If a company has vague CAMs, it might mean their accounting practices are opaque.

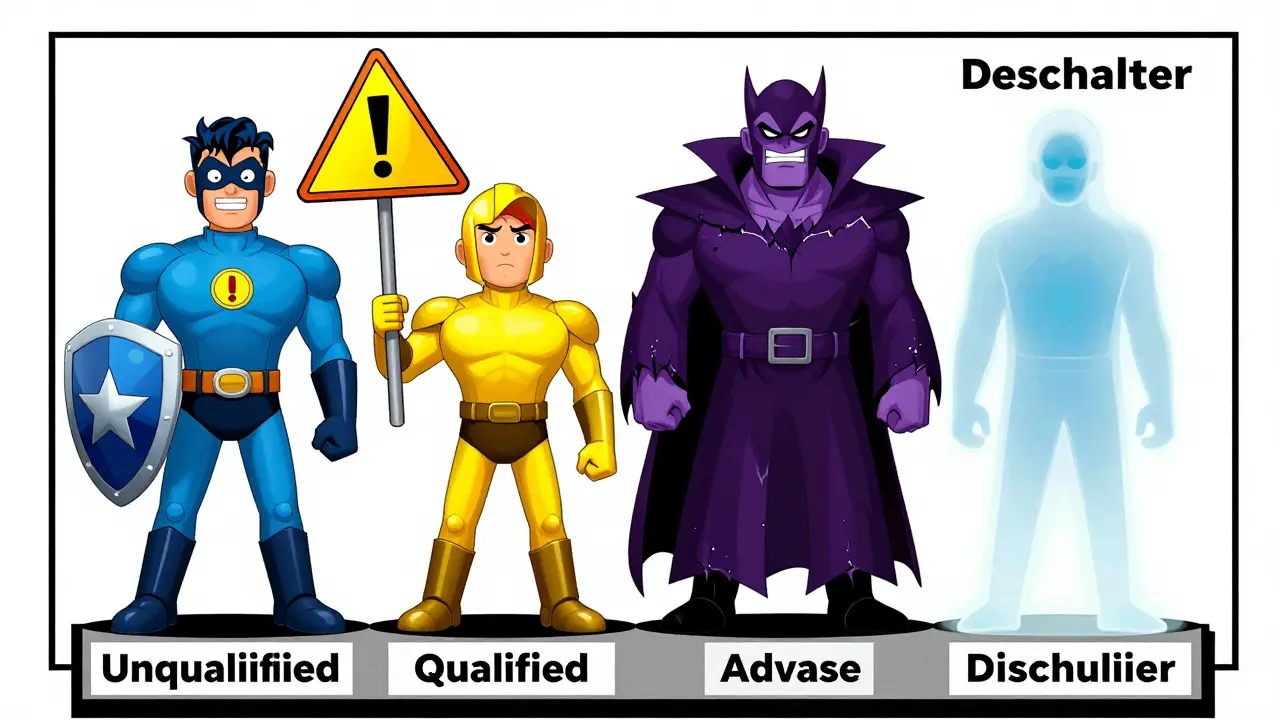

Decoding the Four Types of Audit Opinions

This is the most important part of the entire document. The opinion tells you the bottom line. There are four types, and each carries a different weight. Think of them as grades in school, but with real money on the line.

| Opinion Type | Meaning | Frequency (2023 Data) | Investor Action |

|---|---|---|---|

| Unqualified (Clean) | No material misstatements found. The books are fair. | 82.3% | Safe to proceed. Standard due diligence applies. |

| Qualified | Issues exist, but they are limited to specific areas. Not pervasive. | 12.1% | Caution. Investigate the specific qualified area deeply. |

| Adverse | Significant misstatements. The financials are misleading. | 0.8% | Avoid. High risk of fraud or failure. |

| Disclaimer | Auditor could not form an opinion due to lack of evidence. | 4.8% | Avoid. You cannot trust any number in the report. |

An unqualified opinion is what you want. It means the auditor found no major errors. However, do not assume perfection. A clean opinion only means there are no material misstatements. Small errors might still exist. A qualified opinion is tricky. It often scares investors unnecessarily. For example, a $50,000 error in a $5 billion company might trigger a qualified opinion, but it doesn’t mean the company is failing. Look at the context. An adverse opinion, however, is a hard stop. It means the financial statements do not reflect reality. If you see this, walk away.

The 5 C’s Framework for Analysis

When you dive into the findings section, use the "5 C’s" framework. This method, popularized by Diligent and the Institute of Internal Auditors, helps you evaluate every finding logically. Instead of getting lost in details, ask these five questions for each issue raised in the report.

- Condition: What is the problem? (e.g., "Inventory counts were inaccurate.")

- Criteria: What should have happened? (e.g., "GAAP requires precise inventory valuation.")

- Cause: Why did it happen? (e.g., "Outdated warehouse software.")

- Consequence: What is the impact? (e.g., "$2 million overstated profit.")

- Corrective Action: How will they fix it? (e.g., "Upgrading systems by Q3.")

Most amateur readers stop at the Condition. They see a problem and panic. But the Consequence and Corrective Action tell the real story. If a company identifies a cause and has a solid plan to fix it, that shows strong management. If the consequences are vague or the corrective actions are weak, that is a red flag. In 2023, 67.4% of audit deficiencies cited by regulators involved poor explanation of consequences. If the auditor didn’t explain the impact clearly, the company might be trying to hide the severity.

Red Flags Beyond the Opinion

Even with a clean opinion, you can find trouble. Look for "Explanatory Paragraphs." These are added notes that highlight specific risks. One of the most dangerous is the "Going Concern" paragraph. This appears when auditors doubt the company can stay in business for the next year. In 2023, 76.5% of reports with going concern issues included these paragraphs. If you see this, the company is likely struggling with cash flow or debt.

Another area to watch is Internal Controls. Weaknesses here appear in 38.2% of reports with qualified opinions. If a company cannot control its own books, how can they control their strategy? Also, pay attention to "Emphasis of Matter" paragraphs. These highlight significant events, like a lawsuit or a merger, that don’t change the numbers but affect future performance. In 2023, these made up 22.7% of all explanatory paragraphs. Ignoring them is like ignoring a storm warning while sailing.

Technology and Future Trends

The way we read audit reports is changing. By 2026, technology is making these documents more accessible. The European Financial Reporting Advisory Group (EFRAG) is pushing for digital tagging using XBRL. This allows software to scan reports instantly. Tools like DataSnipper’s Audit Intelligence Platform now process thousands of reports monthly, spotting risks with high accuracy. For individual investors, this means you might soon get AI-driven summaries that highlight key risks automatically.

Regulators are also demanding more transparency. The PCAOB’s updated standards require more detail on Critical Audit Matters. This increases the length of reports but provides deeper insight. As Dr. Carol Pierson from the AICPA noted, static PDFs are giving way to interactive digital reports. This shift helps stakeholders drill down into specific issues without wading through hundreds of pages of text. Keep an eye on these tech-enabled features; they will become standard tools for serious investors.

Practical Steps for Investors

You don’t need a degree in accounting to benefit from this knowledge. Start by downloading the latest 10-K filing for any company you hold stock in. Scroll to the "Auditor’s Report" section. Check the opinion type first. If it’s unqualified, skim the Explanatory Paragraphs. Look for keywords like "going concern," "subsequent event," or "internal control weakness." If you find none, you can likely rest easy. If you find them, dig deeper into the notes. Ask yourself: Is this a one-time issue or a pattern? Does management have a clear plan to fix it?

Remember, an audit report is a snapshot in time. It reflects the past. Use it to assess reliability, not to predict the future alone. Combine it with other metrics like revenue growth and market trends. But never ignore it. As the SEC’s enforcement actions showed, many fraud cases involved companies with warning signs in their audit reports that investors missed. Don’t let that be you.

What is the difference between a qualified and an unqualified audit opinion?

An unqualified opinion means the financial statements are accurate and comply with accounting standards. A qualified opinion means there are specific material misstatements or limitations, but they are not widespread enough to invalidate the entire report. Think of unqualified as a clean bill of health and qualified as a minor illness that needs treatment.

Why do some audit reports have longer lengths than others?

Recent regulatory changes, such as the requirement to disclose Critical Audit Matters (CAMs), have increased report length. Additionally, companies with complex operations, multiple subsidiaries, or significant litigation will have more extensive explanatory paragraphs and notes, leading to longer documents.

What does a 'going concern' warning mean?

A going concern warning indicates that the auditor has substantial doubt about the company's ability to continue operating for the next 12 months. This is a serious red flag, often linked to severe cash flow problems, heavy debt, or loss of major customers.

Can a company have a clean audit opinion and still be fraudulent?

Yes. Audits provide reasonable assurance, not absolute certainty. Auditors sample transactions rather than checking every single one. Sophisticated fraud can sometimes evade detection, especially if it involves collusion among management. However, a clean opinion significantly reduces the risk compared to a qualified or adverse one.

How often should I review an audit report?

For public companies, you should review the annual audit report once a year when the 10-K filing is released. For private investments or partnerships, review it whenever new financial statements are issued. Regular reviews help you catch emerging issues early.