You hold Bitcoin. You’ve traded Ethereum for Solana. Maybe you even mined some Litecoin in your spare time last year. Now, it’s tax season, and the question isn’t just “Do I owe money?” but “How do I pay less without going to jail?” This is where the line gets blurry. On one side, you have tax avoidance, which is using smart, legal strategies to minimize what you owe. On the other, you have tax evasion, which is hiding income from the government. The difference between the two is the difference between a savvy investor and a criminal defendant.

Many people think that because crypto lives on a decentralized blockchain, it’s invisible to tax authorities. That belief is dangerous and outdated. With new regulations rolling out in 2026, the days of flying under the radar are over. Understanding exactly where the legal boundary lies is crucial for protecting your wealth and your freedom.

The Core Difference: Strategy vs. Deception

Let’s clear up the confusion immediately. Tax avoidance is the legal use of the tax regime to your advantage to reduce the amount of tax that is payable by means that are within the law. It involves planning. It involves timing. It involves understanding how the tax code works so you can keep more of your hard-earned money.

Tax evasion is illegal non-payment or underpayment of taxes by misrepresenting financial affairs to the authorities. It involves lying. It involves hiding assets. It involves deleting transaction histories or using privacy coins specifically to obscure your trail from the IRS or your local tax agency.

Think of it this way: If you buy a house and sell it after holding it for more than a year to get a lower capital gains rate, that’s avoidance. If you sell the house and tell the government you never owned it, that’s evasion. In the crypto world, the mechanics are similar, but the complexity is higher because every trade, swap, or reward can be a taxable event.

Why the Norway Study Changes Everything

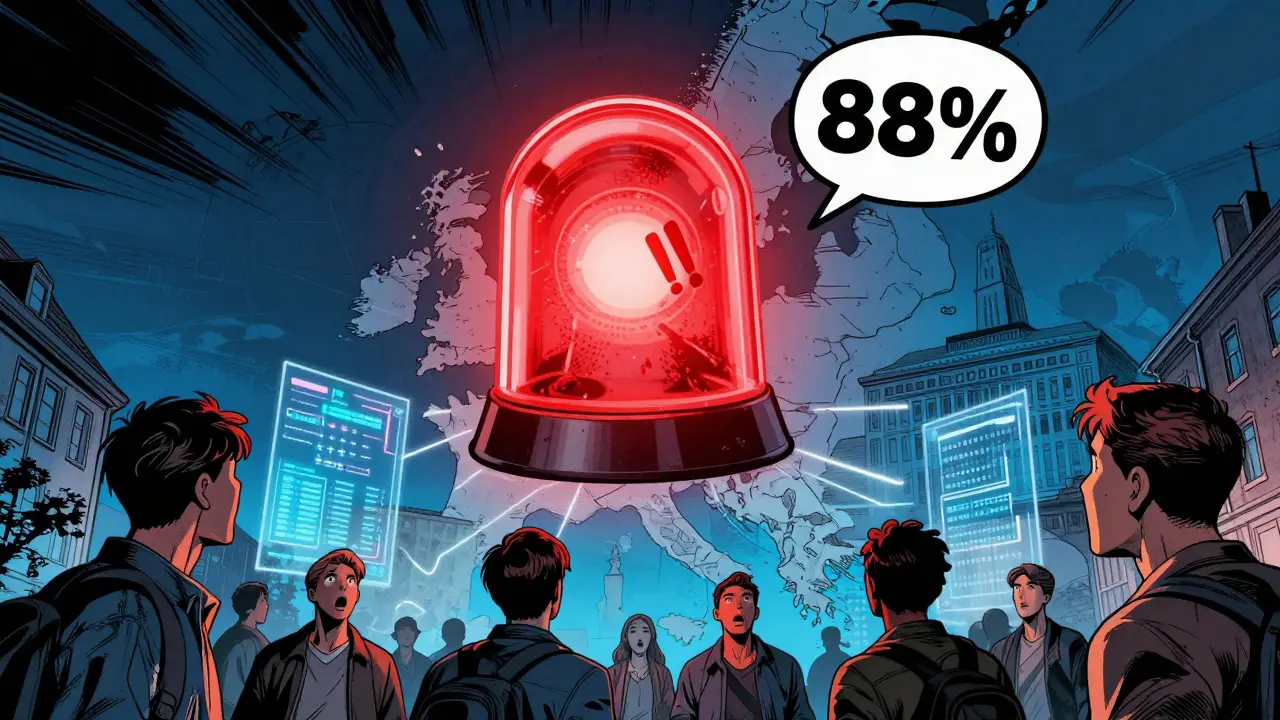

You might feel safe because you haven’t received a letter from the tax man yet. But data suggests otherwise. A comprehensive study conducted in Norway in 2021 revealed a staggering statistic: 88% of crypto holders failed to declare their holdings. This wasn’t a small group; it affected 6% of the entire Norwegian population.

Here is the scary part for those thinking they are hidden: Even investors trading on domestic exchanges that shared identifiable data with the Norwegian Tax Administration showed an 80% noncompliance rate. This proves that simply having data available doesn’t stop people from cheating. However, it also shows that the data is there. The authorities know who holds what. They just need to decide when to act.

The study also highlighted a demographic pattern. Most noncompliers were male, young, and lived in urban areas. If you fit this profile, you might be part of the target audience for future enforcement sweeps. The average value of evaded tax per person ranged between $200 and $1,087. While that seems small individually, multiplied by millions of users, it represents billions in lost revenue. Governments love chasing billions.

Legal Ways to Minimize Your Crypto Tax Bill

Since we want to stay on the right side of the law, let’s talk about legitimate strategies. These methods rely on transparency and proper documentation.

- Hold for the Long Term: In many jurisdictions, including the US, holding an asset for more than one year qualifies it for long-term capital gains rates, which are significantly lower than short-term rates (which are taxed as ordinary income). If you bought Bitcoin in early 2025, selling it in late 2025 triggers short-term rates. Waiting until early 2026 could save you thousands.

- Tax-Loss Harvesting: If you have investments that have gone down in value, you can sell them to realize a loss. This loss can offset gains you’ve made elsewhere. For example, if you made $10,000 in profit on Ethereum but lost $3,000 on a risky altcoin, you can net out that loss to reduce your taxable gain to $7,000. Just watch out for "wash sale" rules, which prevent you from buying back the same asset immediately.

- Utilize Retirement Accounts: In the US, you can hold cryptocurrencies in IRAs or 401(k)s. Gains inside these accounts are tax-deferred (Traditional) or tax-free (Roth), provided you follow contribution limits and withdrawal rules. This is one of the most powerful tools for serious crypto investors.

- Gift Giving: Many countries allow you to gift a certain amount of assets annually without triggering a tax event. Check your local annual exclusion limit. Gifting crypto to a family member in a lower tax bracket can sometimes optimize the overall household tax burden.

These strategies require work. You need to track your cost basis, your acquisition dates, and your disposal events meticulously. There is no magic button, but the savings are real and legal.

The Trap of Illegal Evasion Tactics

So, what does illegal evasion look like in practice? It usually starts with ignorance and ends with fraud. Common tactics include:

- Failing to Report Income: Did you earn staking rewards? Mining payouts? Referral bonuses? These are considered ordinary income in many places. Ignoring them because they arrived in a digital wallet is not a defense; it’s negligence at best, fraud at worst.

- Using Privacy Coins to Hide Trails: Moving funds through Monero or Zcash specifically to break the audit trail is a red flag. While these coins have legitimate privacy uses, using them solely to evade taxes demonstrates intent to defraud.

- Ignoring Wealth Taxes: As seen in the Norway study, some countries tax net wealth, not just income. Failing to declare high-value crypto holdings on annual wealth forms is a direct violation of reporting requirements.

- Underreporting Trades: Trading BTC for ETH is a taxable event. Many traders ignore these "swap" transactions, assuming only selling for fiat counts. This is a massive error. Every disposal of crypto is potentially taxable.

The penalty for evasion is severe. We’re talking about fines that can exceed the tax owed, plus interest, and in egregious cases, prison time. The risk/reward ratio is terrible when you’re risking your freedom to save a few hundred dollars.

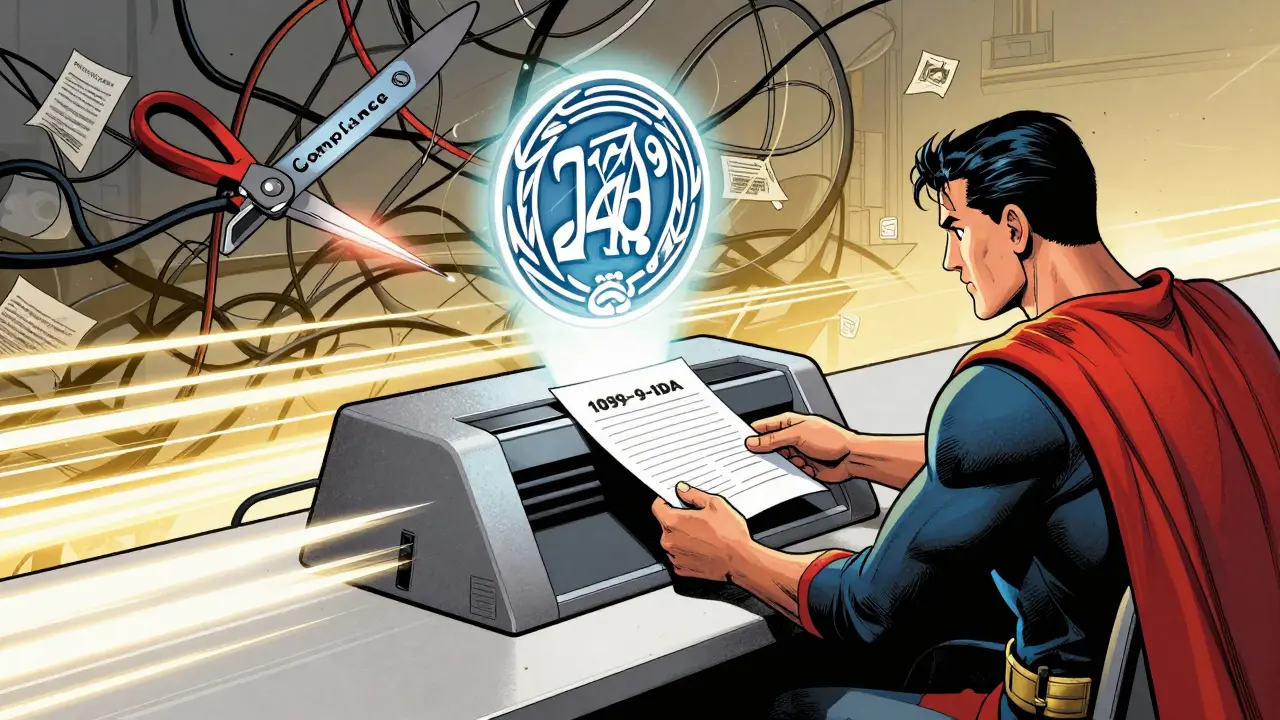

The 2026 Shift: Form 1099-DA and Total Transparency

If you thought 2025 was the start of stricter regulation, wait until 2026. Starting this year, all US cryptocurrency exchanges are required to issue Form 1099-DA a specific IRS form designed to report broker transactions involving digital assets, including capital gains and losses. This form provides the IRS with detailed visibility into your buys, sells, and swaps.

This changes the game completely. Previously, exchanges reported limited information. Now, the IRS will receive data directly from Coinbase, Kraken, Binance.US, and others. They will cross-reference this data with your tax return. If your return says you had zero capital gains, but the 1099-DA shows $50,000 in realized gains, you will get an automated notice. It’s that simple.

This doesn’t just apply to the US. Global cooperation among tax authorities is increasing. The OECD’s Crypto-Asset Reporting Framework (CARF) is being adopted by dozens of countries, creating a global network for sharing crypto transaction data. Hiding behind offshore exchanges is becoming increasingly difficult as KYC (Know Your Customer) standards tighten worldwide.

| Feature | Legal Tax Avoidance | Illegal Tax Evasion |

|---|---|---|

| Legality | Fully compliant with tax laws | Criminal offense (fraud) |

| Transparency | High; all transactions reported accurately | Low; transactions hidden or misrepresented |

| Risk Level | Low; potential for audit questions but defensible | Extremely High; fines, penalties, imprisonment |

| Methods | Long-term holding, loss harvesting, retirement accounts | Unreported income, privacy coin laundering, fake records |

| Future Viability | Increasingly important as regulations tighten | Decreasing due to AI-driven audits and 1099-DA |

Practical Steps for Compliance in 2026

To navigate this new landscape, you need a system. Relying on memory or spreadsheet chaos is no longer sufficient. Here is how to protect yourself:

- Consolidate Your Data: Use professional crypto tax software that connects to your wallets and exchanges via API. Tools like CoinTracker, Koinly, or TokenTax can aggregate years of transaction history and calculate your cost basis automatically.

- Document Everything: Keep records of acquisition dates, purchase prices, and fair market values at the time of each transaction. If you received crypto as payment for services, document the USD value on that day.

- Consult a Professional: Crypto tax law is complex and evolving. A CPA who specializes in digital assets can help you identify legal avoidance opportunities you might miss, such as specific entity structures for mining businesses or charitable donation strategies.

- File Accurately: When you file, ensure your numbers match the 1099-DA forms you receive. If you discover past errors, consider filing an amended return voluntarily before the IRS notices. Voluntary disclosure often reduces penalties.

The era of anonymity is ending. The blockchain is public, and the regulators are catching up. By choosing legal avoidance over illegal evasion, you sleep better at night and keep your assets secure from seizure.

Is trading crypto for other crypto a taxable event?

Yes. In most major jurisdictions, including the US, swapping one cryptocurrency for another (e.g., Bitcoin for Ethereum) is treated as a disposal of the first asset. You must calculate the capital gain or loss based on the difference between your original cost basis and the fair market value of the Bitcoin at the time of the swap.

What happens if I forget to report crypto income?

If you inadvertently fail to report income, it is considered negligence rather than fraud. However, you may still face penalties and interest. The best course of action is to file an amended tax return as soon as you realize the mistake. Voluntary correction often mitigates harsh penalties compared to being caught during an audit.

How does Form 1099-DA affect my tax filing?

Form 1099-DA provides the IRS with detailed records of your capital gains and losses from supported exchanges. You will receive copies of this form, which you must use to reconcile your own records. Discrepancies between your self-reported data and the 1099-DA will likely trigger an automated review or audit request from the tax authority.

Can I use privacy coins legally?

Yes, owning and using privacy coins like Monero is legal. However, using them specifically to conceal transactions from tax authorities can be interpreted as evidence of intent to evade taxes. Ensure that any transfers involving privacy coins are properly documented and reported if they constitute taxable events.

What is the statute of limitations for crypto tax evasion?

In the US, the general statute of limitations for auditing a tax return is three years. However, if you omit more than 25% of your gross income, the window extends to six years. For outright tax evasion (fraud), there is effectively no statute of limitations, meaning the IRS can pursue charges indefinitely.

Sylvia Mossman

June 8, 2026 AT 07:25Another article telling us to just pay up like good little sheep. The system is rigged against the little guy anyway so why should we care about their rules?

Alexander DeVries

June 10, 2026 AT 03:11You need to wake up and smell the coffee Sylvia. Ignoring the law doesn't make you a rebel, it makes you a statistic waiting to happen. The IRS has AI now that catches these patterns instantly. You are playing with fire and pretending it's warm.

Meg Gran

June 10, 2026 AT 11:08Oh look, another moralizing lecture from someone who probably uses TurboTax. The irony is thick enough to cut with a knife. We built this decentralized world to escape exactly this kind of bureaucratic chokehold and here we are reading about how to feed the beast properly. How quaint.

Caitlin Donahue

June 11, 2026 AT 12:05i mean its true tho... my friend got audited last year for not reporting his staking rewards and he lost his house. just saying no harm in being safe i guess

Mark Corpuz

June 11, 2026 AT 21:57The distinction between avoidance and evasion is critical for anyone holding significant assets. Many individuals operate under the false assumption that anonymity on the blockchain equates to invisibility before tax authorities. This misconception is dangerous given the increasing interoperability of global financial data systems. It is prudent to engage with qualified professionals who understand the nuances of digital asset taxation rather than relying on anecdotal evidence from online forums.

Yogendra Dwivedi

June 12, 2026 AT 23:11This is a very comprehensive overview of the current landscape. I appreciate the clarity regarding the Norway study as it highlights the systemic nature of non-compliance rather than isolated incidents. Understanding the demographic trends can help investors anticipate future regulatory focus areas. It seems transparency will be the only viable path forward in the coming years.

Karthikeyan S

June 13, 2026 AT 09:57lol u guys r so scared 😂 just use monero and laugh at the irs they cant trace shit 🤡 stupid gov trying to control everything

Alexis Abster

June 15, 2026 AT 01:04I am truly heartbroken by the fear and anxiety that permeates this community when discussing taxes. It is so important to remember that we are all in this together and that compliance is actually an act of self-care and protection for our families. Let us support each other in navigating these complex waters with kindness and integrity rather than anger or defiance. Your peace of mind is worth far more than any potential savings from evasion.

Dinesh Pattigilli

June 15, 2026 AT 15:32typical red pilled nonsense from the uneducated masses. if you cant handle basic tax compliance you deserve to lose your money. real smart investors know the game and play it right without crying about it. stop whining and do your homework.

Caralee Robertson

June 17, 2026 AT 03:26im from canada and honestly the crypto tax situation here is even more confusing. every time i think i have it figured out they change the rules again. thanks for the info though it helps to see what the us is doing

dan kaffeman

June 18, 2026 AT 01:38Why are we letting foreign entities dictate our financial freedom? The US government is already overreaching but now they want to track every single satoshi movement. This is an invasion of privacy and a step towards total authoritarian control. Americans should resist this encroachment on their rights instead of cowering and filling out forms.

Steven Jacobowitz

June 19, 2026 AT 09:12Wait wait wait hold on. So if I swap BTC for ETH I owe taxes immediately? Even if I dont sell for cash? That seems crazy to me. Like where does the money come from to pay the tax if I still just have crypto? This whole cost basis thing is super confusing and feels like a trap for normal people who just want to trade.

Brad Ranks

June 20, 2026 AT 23:02OMG I literally just realized I haven't reported my DeFi yields from three different protocols since 2021. My heart is racing just thinking about it. Is it too late to fix this? Do I need to hire a lawyer or just pray to the crypto gods? This is a disaster waiting to happen and I feel sick.

Madhu Menon

June 22, 2026 AT 04:15The philosophical implication of state surveillance through blockchain analysis is profound. We traded physical anonymity for digital transparency believing it would liberate us from traditional banking constraints. Instead we have created a perfect ledger for the Leviathan to consume. Perhaps the true value of crypto was never financial but ideological and we have failed to protect that ideal.

Narendra Kulkarni

June 22, 2026 AT 08:04hey everyone hope ur having a good day. just wanted to say that using software like koinly really helped me sort out my mess. its not free but its cheaper than paying penalties. take care of yourselves and stay compliant friends!

verna kennedy

June 23, 2026 AT 10:46If you are smart enough to invest in cryptocurrency you are smart enough to read a tax code. Stop making excuses and start taking responsibility for your actions. The market does not care about your feelings and neither does the IRS. Get your finances in order or get out of the game.

Kelly Tenney

June 25, 2026 AT 06:16Let's create a supportive environment where we can share resources for legal tax planning. No one should feel ashamed for seeking professional help to navigate these complex regulations. Together we can build a community that values both innovation and integrity. Reach out if you need guidance or just someone to listen.

Greg Lewis

June 26, 2026 AT 02:45so basically the government wants a piece of your pie because they didnt invent bitcoin themselves but they still want to profit off it doesnt that sound greedy to you or is it just me who sees the hypocrisy here